Explanation of the accounting equation (assets = liabilities + equity) with real-world examples

Accounting Equation Explained with Real-World Examples

If accounting is the “language of money,” then the Accounting Equation is the “grammar” that ensures everything makes sense. Everything your business owns must come from a source—either through debt from others or through capital provided by the owners. In this article, we explain the accounting equation simply: What are its components? How does every transaction affect its balance? And how do you use it to detect errors in your records early?

- A clear and simple definition of the equation’s three components.

- A visual model (SVG) representing the balance between “What we have” and “Who funded it.”

- Step-by-step analysis of common transactions (Sales, Purchases, Loans).

- A practical example of a “Laundry Shop” starting from scratch to a full equation.

- The relationship between the equation and the Balance Sheet.

- A checklist for confirming the balance of your records.

1) What is the Accounting Equation?

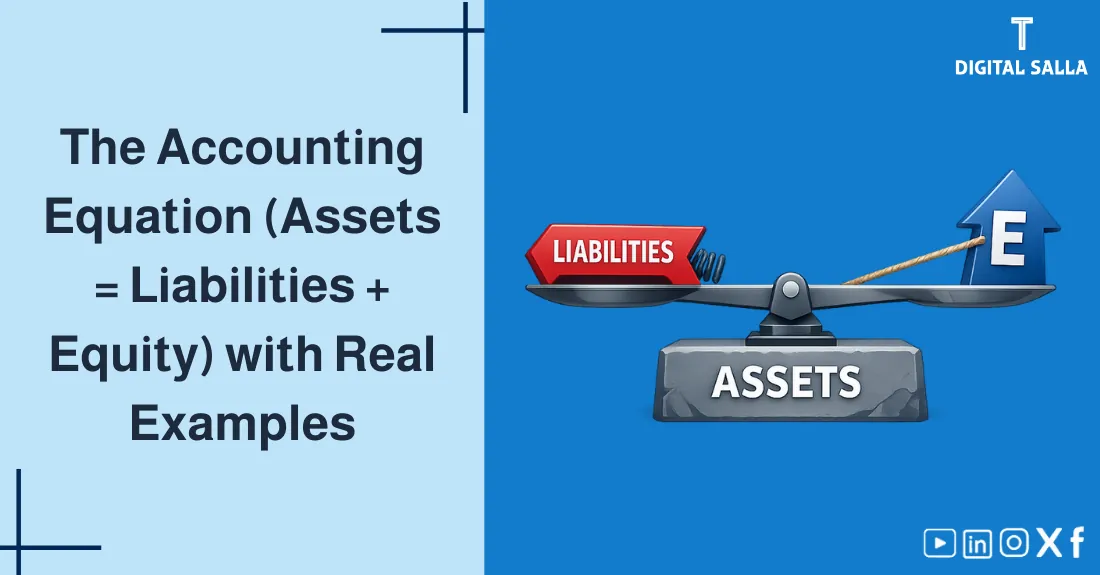

The Accounting Equation (also known as the Balance Sheet Equation) is the foundation of double-entry bookkeeping. It states that the total of what a company owns (Assets) must always be equal to the total of the claims against those assets: claims by creditors (Liabilities) and claims by owners (Equity).

2) The Logic: “Ownership vs. Sources of Funding”

Imagine your company as a “Container.” Everything inside the container (Assets like Cash, Goods, Machines) didn’t appear out of nowhere. It came from one of two sources:

- External Sources (Liabilities): Loans from banks or goods from suppliers not yet paid.

- Internal Sources (Equity): Money provided by you (the owner) or profits retained in the business.

| Assets (The Right Side) | Liabilities + Equity (The Left Side) |

|---|---|

| What the company owns | How these assets were funded |

| Machines, Inventory, Cash, Receivables | Loans, Supplier debts, Owner’s Capital |

3) Deep Dive into the Three Components

A) Assets (What we own)

Economic resources expected to provide future benefit.

- Current: Cash, Bank, Inventory, Accounts Receivable.

- Non-Current: Buildings, Equipment, Vehicles, Furniture.

B) Liabilities (What we owe to others)

Obligations to external parties.

Accounting Guidance Playbook - PDF File

- Short-term: Accounts Payable to suppliers, short-term loans.

- Long-term: Bank loans, mortgages.

C) Owner’s Equity (What we owe to owners)

The residual interest in assets after deducting liabilities.

- Capital: Initial and additional investment by owners.

- Retained Earnings: Profits kept in the company to grow.

4) Visual Representation: The Seesaw

5) Transaction Analysis Rules

Every transaction affects at least two items to keep the balance. Common scenarios include:

- Dual Increase: Buying inventory on credit (+Asset, +Liability).

- Dual Decrease: Paying a loan (-Asset, -Liability).

- Single-Side Shift: Buying equipment with cash (+Asset, -Asset).

6) Practical Example: “Crystal Laundry” Shop

Let’s track Ahmed’s journey in starting his laundry shop:

- Start: Ahmed deposits $50,000 as capital.

(Assets: Cash $50k) = (Equity: Capital $50k) - Loan: He takes a bank loan of $20,000.

(Assets: Cash $70k) = (Liabilities: Loan $20k + Equity: $50k) - Purchase: He buys washing machines for $40,000 cash.

(Assets: Cash $30k + Machines $40k) = (Liab: $20k + Equity: $50k)

| Transaction | Assets | Liabilities | Equity | Balance? |

|---|---|---|---|---|

| Opening Capital | 50,000 | 0 | 50,000 | ✅ 50 = 50 |

| Bank Loan | 70,000 | 20,000 | 50,000 | ✅ 70 = 70 |

| Buying Machines | 70,000 | 20,000 | 50,000 | ✅ 70 = 70 |

8) Relation to the Balance Sheet

The Balance Sheet is literally just a snapshot of the accounting equation at a specific point in time. It is structured exactly like the equation:

- The top half (or left side) lists all Assets.

- The bottom half (or right side) lists all Liabilities and Equity.

9) How to detect errors using it?

The equation is a powerful diagnostic tool. If your records show:

- Total Assets ≠ Liabilities + Equity: There is definitely an error in recording or posting.

- Typical causes: Forgetting one side of a transaction, doubling one side, or error in calculation.

11) Frequently Asked Questions

What is the accounting equation simply?

It is the rule that what you own (Assets) equals what you owe to others (Liabilities) plus your own money (Equity).

Can Equity be negative?

Yes, if the company’s total losses exceed its capital, meaning liabilities are greater than assets.

12) Conclusion

Mastering the Accounting Equation is not about memorizing a formula; it is about understanding the DNA of your business. Every machine you buy and every penny you spend must have a source. By keeping this equation in mind, you will ensure that your records are accurate, your financial statements are balanced, and your business decisions are based on solid truth.