Job Costing System: How to Calculate the Profitability of Each Project or Order Individually?

Job Order Costing: How to Calculate the Profitability of Each Project or Order Individually?

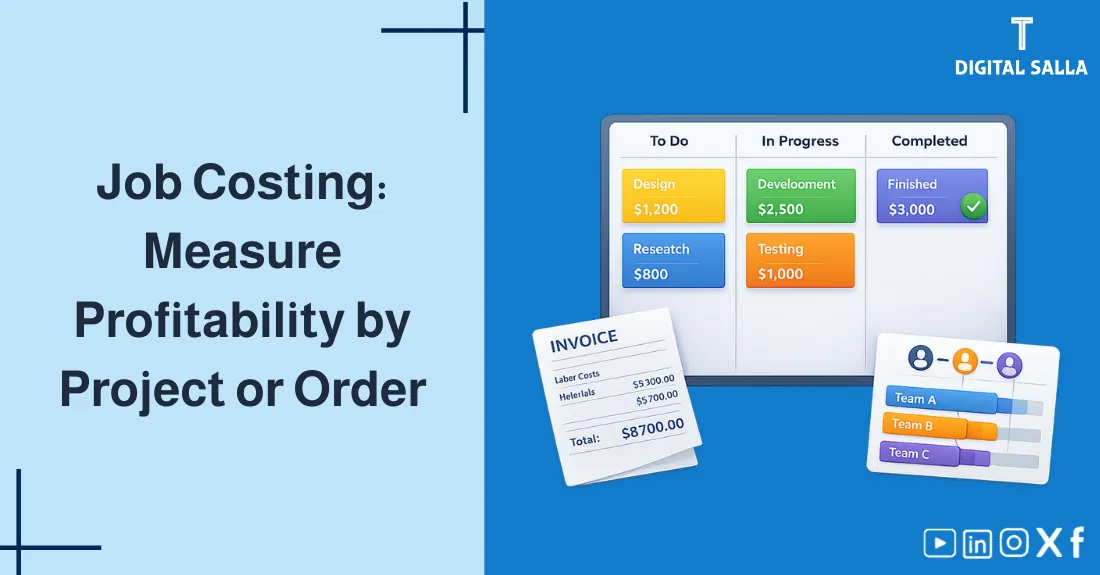

Job Order Costing: How to calculate the cost of an order and the profitability of each project separately using a Job Cost Sheet, with steps for accurate aggregation of materials, labor, and overhead—Digital Salla.

- What is Job Order Costing and which industries use it?

- The Job Cost Sheet: The ultimate document for project control.

- Steps to accumulate costs: Direct Materials, Direct Labor, and Applied Overhead.

- Accounting flow from Work-in-Process (WIP) to Finished Goods.

- How to calculate Project Profitability and analyze variances per order.

1) The Concept of Job Order Costing

Job Order Costing is a costing system used by companies that produce unique, custom products or distinct batches of items. Unlike mass production, where costs are averaged, Job Costing treats every order as an independent financial entity.

- Target Industries: Construction, custom furniture, printing shops, legal firms, advertising agencies, and aircraft manufacturing.

2) The Job Cost Sheet: Anatomy & Components

The Job Cost Sheet is the “Master Ledger” for a single project. It accumulates costs as the work progresses through departments.

3) Recording Direct Materials (DM)

Materials are charged to a job via a Materials Requisition Note.

- Source: Warehouse requests.

- Verification: Ensure the “Job ID” is clearly written on the request to prevent material cross-contamination between orders.

4) Recording Direct Labor (DL)

Labor costs are assigned using Time Tickets or digital activity logs.

FX Revaluation & Translation Toolkit - Excel File

- Rule: Only Direct Labor (hands-on time) is recorded on the sheet. Factory supervisors and cleaners are handled via Overhead.

- Accuracy Check: Total hours on job sheets must reconcile with the Payroll Register for the period.

5) Applying Manufacturing Overhead (MOH)

Since actual overhead (rent, utilities) isn’t known until the end of the month/year, we use a Predetermined Overhead Rate to “Apply” costs to jobs in real-time.

- Formula: Applied Overhead = POHR × Actual Activity (e.g., Labor Hours).

6) The Flow of Costs through Jobs

Costs move through the system as the job physically moves through the factory:

- WIP Inventory: Accumulates costs while the job is “Active.”

- Finished Goods: When the job is “Completed.”

- COGS: When the job is “Delivered/Sold” to the customer.

7) Calculating Individual Order Profitability

The ultimate goal of Job Order Costing is the Profitability Report per Order.

| Element | Value | Management Insight |

|---|---|---|

| Selling Price | $20,000 | Agreed contract value. |

| Direct Manufacturing Cost | ($13,300) | Sum of DM, DL, and Applied MOH. |

| Gross Profit | $6,700 | Project Margin (33.5%). |

| Estimated Period Costs | ($2,000) | Selling & Admin share (allocated). |

| Net Project Profit | $4,700 | Final profitability for this client. |

8) Operational Controls & Readiness Checklist

To ensure your project costing is reliable:

Job Costing Quality Gate

- Are materials withdrawn only with a Job ID?

- Do workers record time as they work (Real-time logs)?

- Is the overhead rate reviewed whenever a major cost changes (e.g., new lease)?

- Do we perform “Post-Job Reviews” to compare actual costs with the original estimate?

- Are Job Sheets locked once the order is delivered to prevent retroactive edits?

9) Common Errors and How to Prevent Them

- Material Transfers: Taking left-over materials from Job A to use on Job B without a “Transfer Note.”

- Idle Time: Charging “Machine downtime” to a specific job (it should be an indirect overhead cost).

- Outdated Rates: Using a 2023 overhead rate for 2025 projects.

- Incomplete Costing: Forgetting to include specialized freight or subcontracting costs specific to a job.

10) Frequently Asked Questions

What is Job Order Costing?

It is a system that accumulate costs for each individual order or project separately, suitable for custom or batch-based businesses.

Why use “Applied” overhead instead of “Actual”?

Because managers need to know the cost immediately to price the job and invoice the client, they cannot wait for the monthly utility bill to arrive.

Is Job Costing used in service businesses?

Yes. Law firms, audit firms, and consultancies use “Engagement Costing,” which is a variation of Job Costing where the primary cost is “Billable Hours.”

11) Conclusion

Mastering Job Order Costing is the key to identifying your “Winning” and “Losing” projects. By maintaining disciplined Job Cost Sheets, accurately tracing Direct Costs, and applying Overhead consistently, you move from “Global Profitability” to “Granular Visibility.” This allows you to refine your bidding process and focus your resources on the most profitable segments of your business.

Action Step Now (30 minutes)

- Open your Work-in-Process (WIP) ledger.

- Select one active job and check if all material requisitions are attached.

- Compare the actual labor hours spent on that job so far with your initial budget.