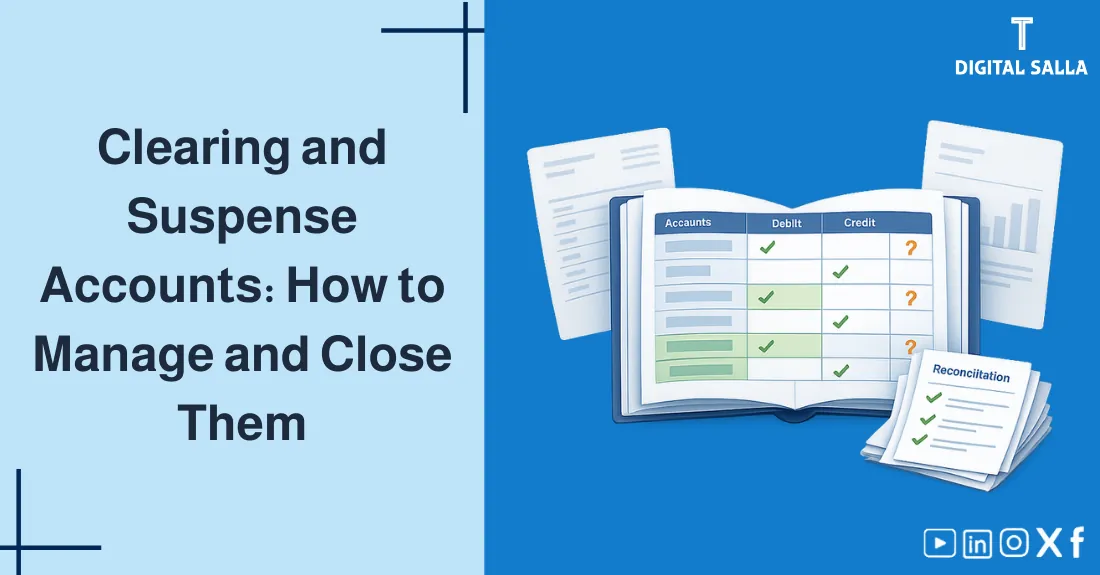

Intermediate Accounts (Clearing Accounts) and Suspense Accounts: How to Manage and Close Them?

Clearing Accounts (Clearing Accounts) and Suspense Accounts: How to Manage and Close Them?

In any accounting system, there are amounts that represent “transit points” rather than final destinations. Clearing Accounts help organize the matching between different sources, while Suspense Accounts act as a temporary “parking spot” for unknown transactions. However, if these accounts are not managed with a “Zero-Balance” strategy, your Trial Balance will become cluttered with old, ambiguous figures. In this guide, we provide a practical framework for managing and clearing these accounts professionally.

- A clear definition of Clearing Accounts and their planned roles.

- What are Suspense Accounts and why do they appear?

- A quick comparison table between the two types.

- Visual model (SVG) explaining the clearing journey from bank to ledger.

- Strategies for Trial Balance Cleanup and handling unallocated payments.

- How to use Aging Reports for transit accounts.

- A checklist for month-end and year-end closing.

1) Defining Clearing vs. Suspense Accounts

Both are Temporary Accounts used to record amounts until they can be posted to their permanent accounts. However, the reason for their existence is different:

- Clearing Account: A planned account used to facilitate the matching of two sides of a transaction that don’t happen simultaneously (e.g., Bank Clearing).

- Suspense Account: An unplanned account used to “park” an amount when you don’t know where it belongs (e.g., an incoming transfer with no customer name).

2) Summary Comparison Table

| Feature | Clearing Account | Suspense Account |

|---|---|---|

| Purpose | Internal Matching & Control | Investigating Unknown Entries |

| Origin | Planned in the system design | Created to solve an immediate mystery |

| Example | Payroll Clearing, POS Clearing | Unidentified Bank Inflow |

| Ideal Balance | Zero (at the end of process) | Zero (as soon as resolved) |

3) Clearing Accounts: The Planned Buffer

In modern ERP systems, clearing accounts are essential for Internal Control.

Accounting Templates Library - Excel & Word Files

Ready-to-Use Accounting Templates Library: A comprehensive library of professional Excel templates—c...

4) Suspense Accounts: Investigating Ambiguity

A suspense account is your “Waiting Room.” It is used when an accountant is under pressure to close a day or a month but lacks complete info for a specific entry.

5) Visual Journey: The Transit Point

6) Aging Reports for Transit Accounts

Just like you track Accounts Receivable Aging, you must track the aging of clearing/suspense accounts.

- 0-7 Days: Normal operational delay.

- 7-30 Days: Warning (Needs follow-up).

- +30 Days: High Risk (Indicates a lost document or a breakdown in the cycle).

7) Strategies for Zero-Balance Closing

- Weekly Reconciliation: Don’t wait for month-end to clear transit accounts.

- Responsibility Assignment: Assign one person to be the “investigator” for the suspense account.

- Threshold Rule: If an amount remains in suspense for more than 90 days despite investigation, escalate to management for write-off or special adjustment.

8) Common Management Mistakes

- Hiding Losses: Recording a deficit as a “debit balance” in a suspense account instead of an expense.

- Ignoring Credits: Leaving unknown cash inflows in suspense without attempting to identify the customer (Lost Revenue).

- Reporting as Assets: Listing a large clearing balance as an “Asset” on the Balance Sheet without disclosure.

9) Frequently Asked Questions

How often should I clear the suspense account?

Daily or weekly is best. It should never have a balance by the time you issue your monthly financial statements.

Is “Cash in Transit” a clearing account?

Yes, it is a classic example of a clearing account used to track money that has left the safe but hasn’t reached the bank yet.

10) Conclusion

Clearing and Suspense accounts are powerful tools for organization, but only if they remain temporary. By adopting a “Zero-Balance” culture and using aging reports to track transit items, you ensure that your financial statements remain accurate, transparent, and ready for audit at any time.