Interim Financial Reports (IAS 34): How Do Quarterly Statements Differ from Annual Ones?

Interim Financial Reports According to IAS 34: What Is the Difference Between Quarterly and Annual Statements? And What Are the Key Interim Disclosure Requirements and How to Summarize Information Without Compromising Transparency or Comparability—Digital Basket.

Related Parties: How to Identify and Disclose Them According to IAS 24

Related Parties: How to Identify Related Parties and Related Party Transactions, and What Are the Disclosure Requirements According to IAS 24 to Avoid Conflicts of Interest and Improve Report Transparency for the Auditor and Investor—Digital Basket.

Subsequent Events (IAS 10): Corona as a Model, When to Adjust the Statements and When to Disclose Only?

Subsequent Events According to IAS 10: The Difference Between Adjusting and Non-Adjusting Events (Events After Reporting Period), and When to Adjust the Statements and When to Disclose Only, with Examples Like Corona—Digital Basket.

Accounting Policies and Notes: How to Write Disclosures that Protect the Company and Clarify the Picture?

Notes to Financial Statements: How to Write Clear Financial Disclosures and Details of Statements that Protect the Company and Explain the Numbers to the Reader and Auditor, with a Practical Structure for Notes—Digital Basket.

Preparing Cash Flows Practically: How to Extract Them from the Balance Sheet and Income Statement? (Step by Step)

Preparing the Cash Flow Statement Practically Step by Step: Extracting it from the Balance Sheet and Income Statement, Converting Accruals to Cash Using a Flow Worksheet, with Explanation of Direct and Indirect Methods—Digital Basket.

Cash Flow Statement (IAS 7): Direct vs Indirect Method (Which to Choose?)

Cash Flow Statement According to IAS 7: Comparison of Direct vs Indirect Method, and How to Present the Cash Flow Statement for Operating, Investing, and Financing Activities to Understand True Liquidity—Digital Basket.

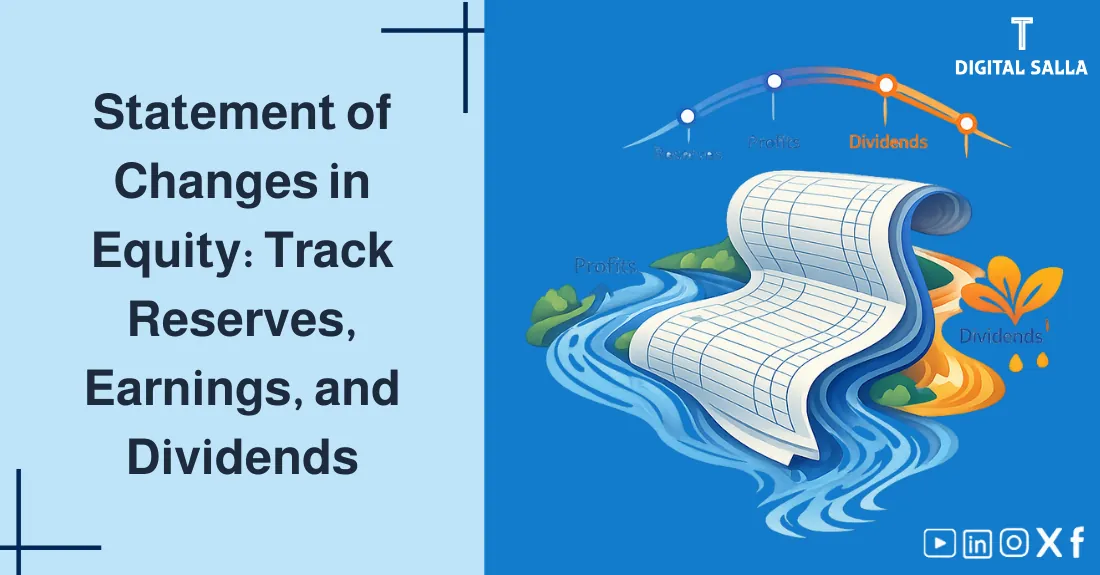

Statement of Changes in Equity: Track the Movement of Reserves, Earnings, and Share Distributions

Statement of Changes in Equity: How to Track the Movement of Capital, Reserves, and Retained Earnings, and Document Dividend Distributions and Share Changes to Explain What Happened in Equity During the Period—Digital Basket.

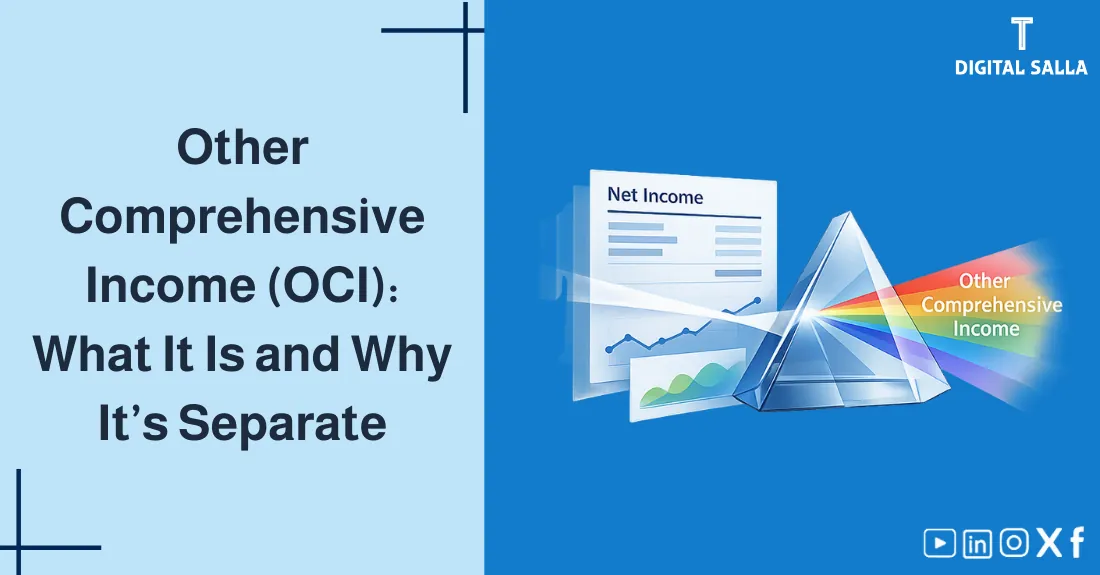

Other Comprehensive Income (OCI): What is it? And Why Do Its Items Not Appear in the Profit and Loss Statement?

Other Comprehensive Income (OCI): What is it? And Why Are Some Items Presented Outside the Profit and Loss Statement? Learn About Comprehensive Income Items Like Currency Differences and Revaluation and Their Impact on Equity—Digital Basket.

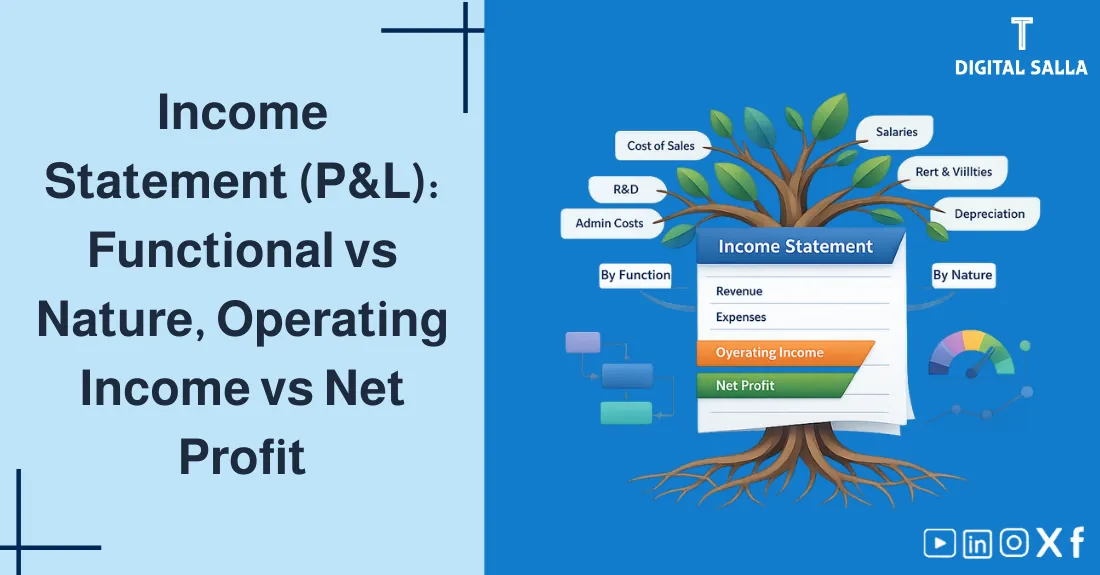

Income Statement (P&L): Functional vs Nature Classification, and the Difference Between Operating Income and Net Profit

Income Statement (P&L): The Difference Between Functional and Nature Classification, and How to Distinguish Operating Income from Net Profit, with an Explanation of Revenues and Expenses for Clear Reading of the Profit and Loss Account—Digital Basket.

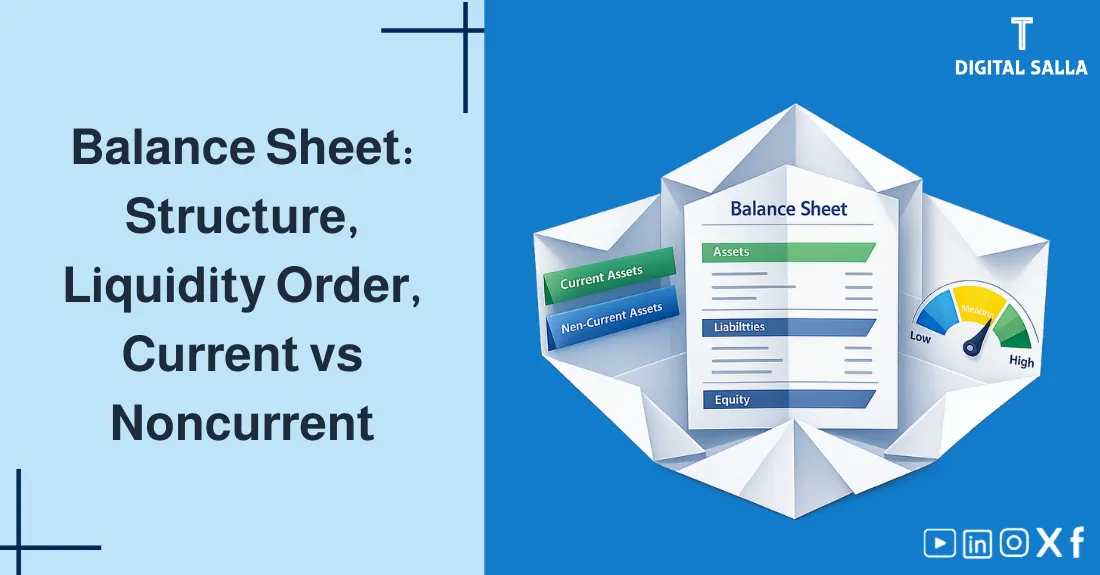

Balance Sheet: Structure, Liquidity Order, and the Difference Between Current and Non-Current

Balance Sheet: Explanation of the Balance Sheet and Its Structure and Liquidity Order, and How to Differentiate Between Current and Non-Current in Assets, Liabilities, and Equity for Proper Reading—Digital Basket.

Preparation and Presentation of Financial Statements According to International Standards (IAS 1): The Complete Guide

Preparation of Financial Statements According to IAS 1: A Comprehensive Guide to the Structure of Financial Reports, from Final Accounts to Audited Financial Statements, with Presentation, Classification, and Disclosure Rules Expected by Auditors—Digital Basket.

Materiality: When to Ignore the Error and When to Adjust It?

Materiality: How to Determine Materiality? And When Can an Insignificant Error be Ignored, and When Does it Become a Material Error Requiring Adjustment and Financial Disclosure to Protect Credibility—Digital Basket.

Correcting Accounting Errors: Should You Adjust Retrospectively or in the Current Period?

Correcting Accounting Errors According to IAS 8: When Should Previous Years be Retrospectively Adjusted? And When is it Sufficient to Adjust in the Current Period? Explanation of Restating Financial Statements and Disclosure Steps to Avoid Risks—Digital Basket.

Accounting Estimate vs Accounting Policy: Fundamental Difference and How to Address

Accounting Estimate vs Accounting Policy: What is the Fundamental Difference? And How to Address Changes in Accounting Estimates like Useful Life and Provisions Without Violating Standards or Misleading Results—Digital Basket.

How to Write an Accounting Policies Guide for the Company? (With a Proposed Model)

Accounting Policies Guide: Steps to Prepare a Policies Guide and Link it to Financial Procedures and Corporate Governance, with a Proposed Model to Help You Standardize Financial Policies and Reduce Disputes During Review—Digital Basket.