Users of Accounting Information (Stakeholders): What Do the Bank, Investor, and Management Want?

Users of accounting information differ in their needs: stakeholders such as banks, investors, and management, and how external and internal reports meet their expectations—Digital Basket.

Accounting Documents: Invoice, voucher, and notice (Tax Acceptance Conditions)

Accounting Documents Guide: Tax invoice, receipt voucher, payment voucher, and notices, with tax acceptance conditions and best practices for document cycle and archiving to ensure compliance—Digital Basket.

Characteristics of Good Accounting Information: Relevance and Reliability (Conceptual Framework Explanation)

Learn the characteristics of accounting information according to the conceptual framework: relevance, reliability, and comparability, and how to enhance the quality of financial reports for better decision-making—Digital Basket.

Accounting Errors in Entries: Deletion, Duplication, and Misdirection (How to Detect Them?)

Learn about accounting errors in entries such as deletion errors, duplication errors, and misdirection errors, and how errors are detected through review, posting, and trial balance with practical solutions—Digital Basket.

Accounting Branches: A Guide to Choosing Your Specialty (Financial, Cost, Tax, Audit)

Discover the branches and types of accounting, and choose the most suitable accounting specialties: financial, cost, tax, audit, with an explanation of the difference between financial and managerial accounting—Digital Basket.

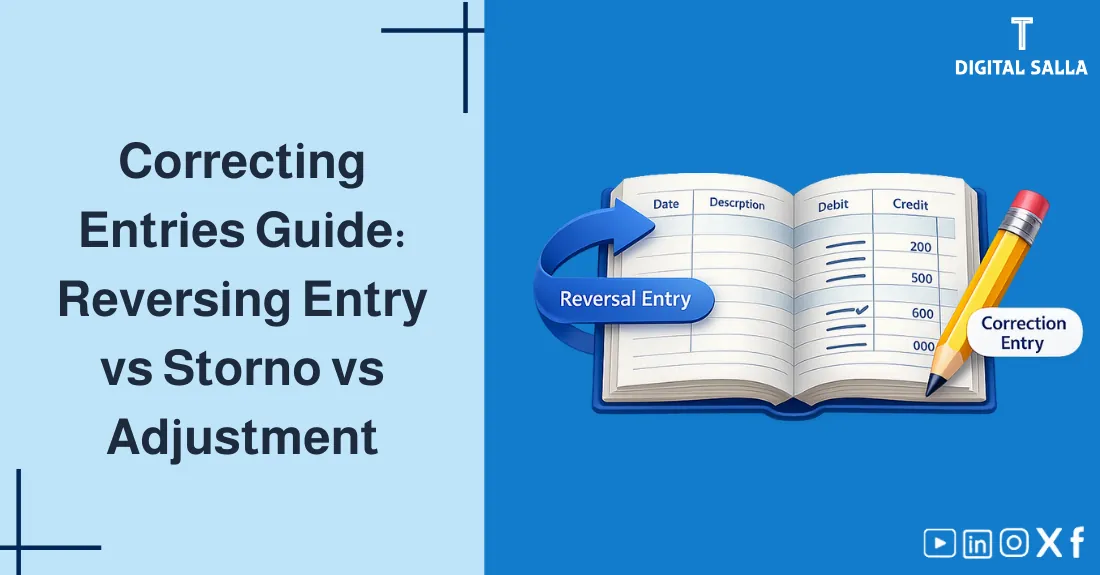

Methods for Correcting Wrong Entries: Reversing Entry vs Correction Entry (Storno)

Correcting Accounting Entries: When to use a reversing entry and when to use a correction entry (Storno)? Explanation of the detailed and concise method with examples to help you adjust the entry without distorting reports—Digital Basket.

The Accounting Equation and the Logic of Debits and Credits

Learn the Accounting Equation and the Logic of Debits and Credits: The Balance Sheet Equation (Assets Equal Liabilities and Equity) with a Simplified Explanation Linking Transactions to Their Impact—The Digital Basket.

Account Classification Guide and Entry Direction: Assets, Liabilities, and Equity

Account Classification Guide: Categorizing accounts and building an account structure linking assets, liabilities, and equity to financial statement elements, with rules for directing entries for correct recording from the first time—Digital Basket.

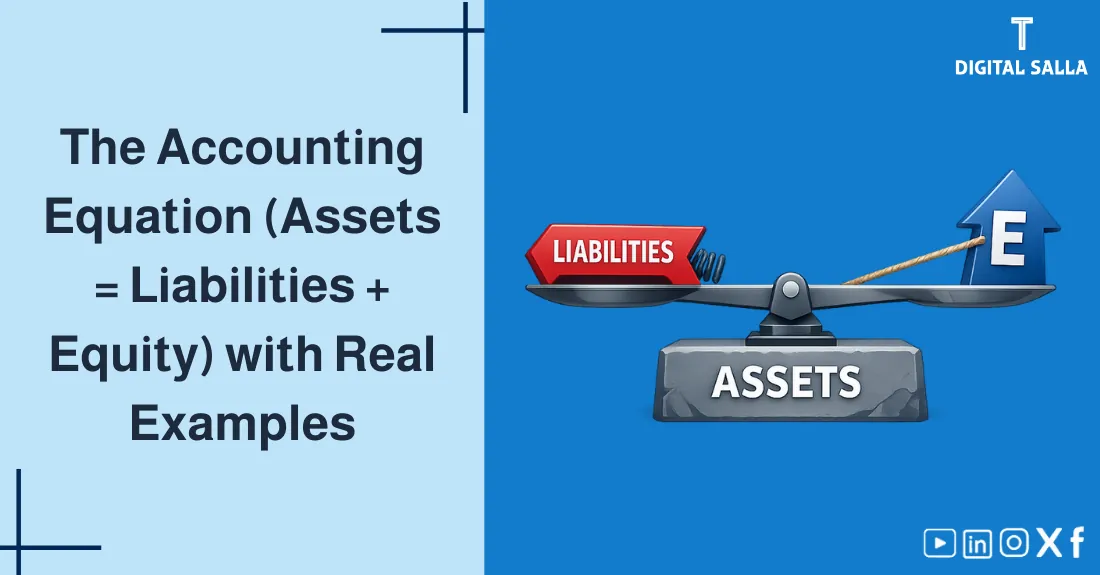

Explanation of the accounting equation (assets = liabilities + equity) with real-world examples

Explanation of the accounting equation with assets = liabilities + equity through real-world examples of the accounting equation, and how to maintain the balance of the equation and understand the impact of transactions instantly—Digital Basket.

Chart of Accounts (COA) Design: How to Build a Flexible Account Tree for a Startup or Large Company?

Chart of Accounts Guide: How to design a flexible account tree and a COA structure that can grow? Learn account coding and best practices for a startup or large company for more accurate reports—Digital Basket.

Debit vs Credit rule: How to understand it without memorization?

Understand the Debit and Credit rule without memorization: the difference between debit and credit with the logic of giving and taking, linking it to the nature of accounts and easy entry examples—Digital Basket.

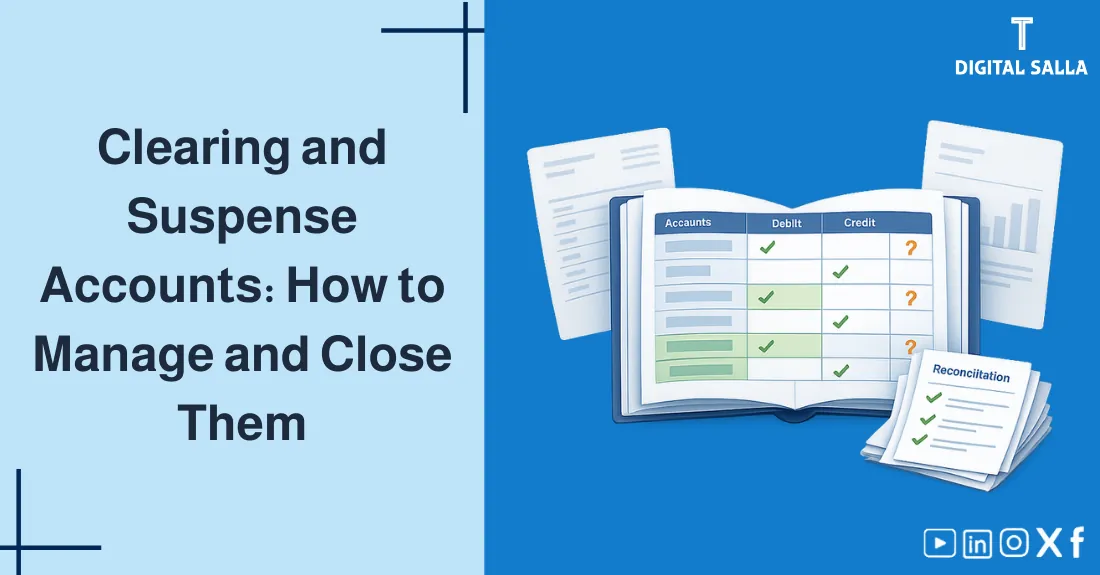

Intermediate Accounts (Clearing Accounts) and Suspense Accounts: How to Manage and Close Them?

Intermediate Accounts Guide: When to use Clearing Accounts and Suspense Accounts? And how to manage and close temporary accounts through account reconciliation to avoid hanging balances—Digital Basket.

Nature of accounts (Normal Balance): Why are assets debited and liabilities credited?

Nature of accounts or normal balance: Why are assets debited and liabilities credited? Explanation of debited accounts and credited accounts and entry rules and their relation to the chart of accounts—Digital Basket.

Contra Accounts: Accumulated Depreciation and Allowance for Doubtful Accounts (Explanation and Application)

Learn about Contra Accounts such as Accumulated Depreciation and Allowance for Doubtful Accounts, and how to calculate and correctly present the net book value in statements—Digital Basket.

Collection vs Revenue: Why is cash not always profit?

Learn the difference between collection and revenue and why cash is not always profit: revenue recognition according to the accrual principle and distinguishing between cash flow vs profit with examples—Digital Basket.