Matching Principle: The Concept Governing Inventory Adjustments

Matching Principle: How to match revenues with expenses to ensure the independence of financial years? An explanation of why this principle governs inventory adjustments and prevents profit inflation—Digital Basket.

Other Comprehensive Income (OCI): What is it? And Why Do Its Items Not Appear in the Profit and Loss Statement?

Other Comprehensive Income (OCI): What is it? And Why Are Some Items Presented Outside the Profit and Loss Statement? Learn About Comprehensive Income Items Like Currency Differences and Revaluation and Their Impact on Equity—Digital Basket.

Accruals and Prepayments: Adjustments and Precise Processing

Accruals and Prepayments: Explanation of Accruals and Prepayments, adjusting entries, precise processing, and how they are classified between current assets and liabilities to ensure accurate results—Digital Basket.

Statement of Changes in Equity: Track the Movement of Reserves, Earnings, and Share Distributions

Statement of Changes in Equity: How to Track the Movement of Capital, Reserves, and Retained Earnings, and Document Dividend Distributions and Share Changes to Explain What Happened in Equity During the Period—Digital Basket.

Accrued and Deferred Revenue: How to Prevent Profit Inflation or Conceal Liabilities?

Accrued and Deferred Revenues: The difference between Accrued Revenue and Deferred Revenue, and how to prevent profit inflation or conceal liabilities resulting from contracts through correct entries and clear disclosure—Digital Basket.

Cash Flow Statement (IAS 7): Direct vs Indirect Method (Which to Choose?)

Cash Flow Statement According to IAS 7: Comparison of Direct vs Indirect Method, and How to Present the Cash Flow Statement for Operating, Investing, and Financing Activities to Understand True Liquidity—Digital Basket.

Depreciation Entries: Calculation, Recording, and Impact on Profit

Depreciation Entries: How to calculate and record depreciation expense with accumulated depreciation, and compare depreciation methods like straight-line, and how this reflects on profit and financial statements—Digital Basket.

Preparing Cash Flows Practically: How to Extract Them from the Balance Sheet and Income Statement? (Step by Step)

Preparing the Cash Flow Statement Practically Step by Step: Extracting it from the Balance Sheet and Income Statement, Converting Accruals to Cash Using a Flow Worksheet, with Explanation of Direct and Indirect Methods—Digital Basket.

End-of-Period Inventory Adjustments: Shortages, Damaged Goods, and Price Declines (NRV)

End-of-Period Inventory Adjustment: Inventory count and handling of shortages, surpluses, and damaged goods, and how to evaluate inventory and create a provision for inventory write-down according to NRV to avoid unreal profits—Digital Basket.

Accounting Policies and Notes: How to Write Disclosures that Protect the Company and Clarify the Picture?

Notes to Financial Statements: How to Write Clear Financial Disclosures and Details of Statements that Protect the Company and Explain the Numbers to the Reader and Auditor, with a Practical Structure for Notes—Digital Basket.

Currency Differences (FX Revaluation): Re-evaluating Foreign Balances Before Closing

Currency Differences: FX Revaluation Guide for re-evaluating currencies and foreign currency balances before closing, and how to correctly record exchange gains and losses to avoid profit surprises—Digital Basket.

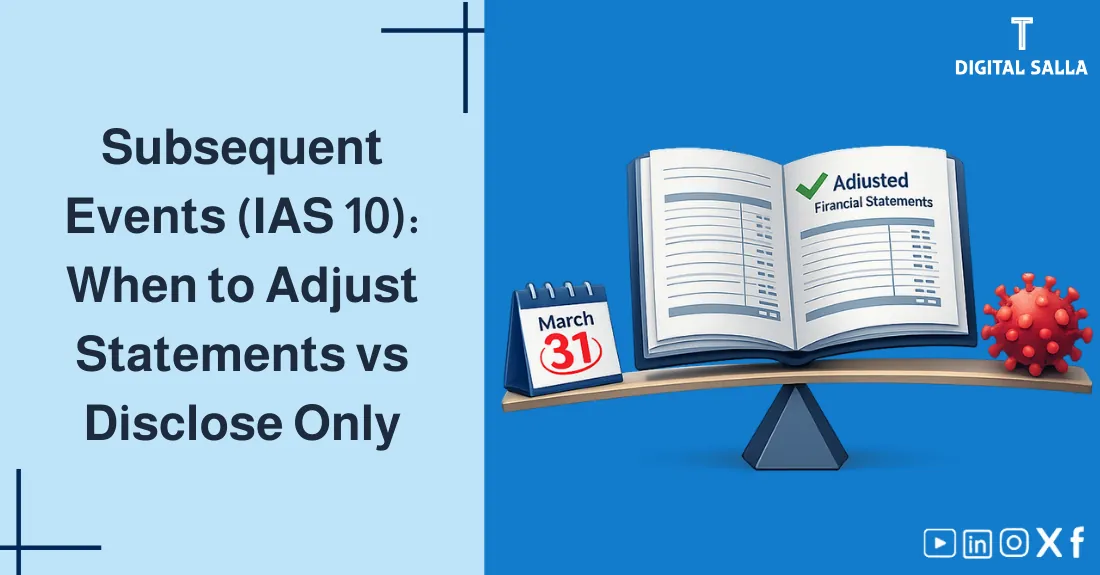

Subsequent Events (IAS 10): Corona as a Model, When to Adjust the Statements and When to Disclose Only?

Subsequent Events According to IAS 10: The Difference Between Adjusting and Non-Adjusting Events (Events After Reporting Period), and When to Adjust the Statements and When to Disclose Only, with Examples Like Corona—Digital Basket.

Generally Accepted Accounting Principles (GAAP) vs International Standards (IFRS): Key Differences

Explanation of the difference between GAAP and IFRS and the key differences between generally accepted accounting principles and international accounting standards, and when transitioning to international standards is beneficial—Digital Basket.

The Origin of International Standards (IFRS/IASB): Why Did the World Decide to Unify the Language of Money?

Explanation of the Origin of International Standards IFRS and the Role of IASB and the History of the International Standards Committee, and Why Financial Globalization Led to the Unification of Accounting Standards as a Common Language—The Digital Basket.

Asset or Expense? Capitalization Rules and How to Decide?

The difference between an asset and an expense: Capitalization rules and how to distinguish between capital and revenue expenditures according to IAS 16, with practical questions to help you make the correct classification decision—Digital Basket.

Liability vs Provision vs Contingent Liability: Key Differences and Their Impact on Statements

Understand the difference between provision, liability, and contingent liability according to IAS 37: Provisions vs Liabilities, and when to recognize provisions or just disclose them, and their impact on financial statements—Digital Basket.

The Difference Between Reserves, Retained Earnings, and Provisions: Untangling the Confusion

Explain the difference between reserves, provisions, and retained earnings: What are the types of reserves and statutory reserve? And how does profit distribution affect equity and performance indicators—Digital Basket.

Operating Revenues vs Gains: Why should they be separated in the income statement?

Revenue and gains are not the same thing: the difference between Revenue and Gain and how to separate operating and non-operating revenues from asset sale gains for accurate income statement analysis—Digital Basket.

Cost of Goods Sold (COGS) vs Operating Expenses (OPEX): Correct classification rules

The difference between Cost of Goods Sold and Expenses: COGS vs OPEX and how classification affects gross profit margin and the classification of costs and administrative expenses, with examples to prevent profit distortion—Digital Basket.